Choosing the right financial safety net is one of the most critical decisions you can make to protect your household income. When you start researching your options in the UK, one brand name is practically unavoidable: Aviva. As one of the largest and most established insurance providers in the country, millions of Britons trust them with their cars, homes, and lives.

However, brand recognition alone is never a good enough reason to sign a financial contract. If you are a self-employed tradesperson, a primary breadwinner, or someone who leads an active lifestyle, you need to know exactly what is written in the fine print. You need to know if Aviva personal accident insurance genuinely holds up to scrutiny when you need it most.

In this comprehensive, objective review, we strip away the marketing jargon. We will examine exactly how Aviva structures its accident cover, the specific injuries that trigger a payout, the hidden exclusions you must be aware of, and whether this policy is the right fit for your specific lifestyle.

Table of Contents

What is Aviva personal accident insurance?

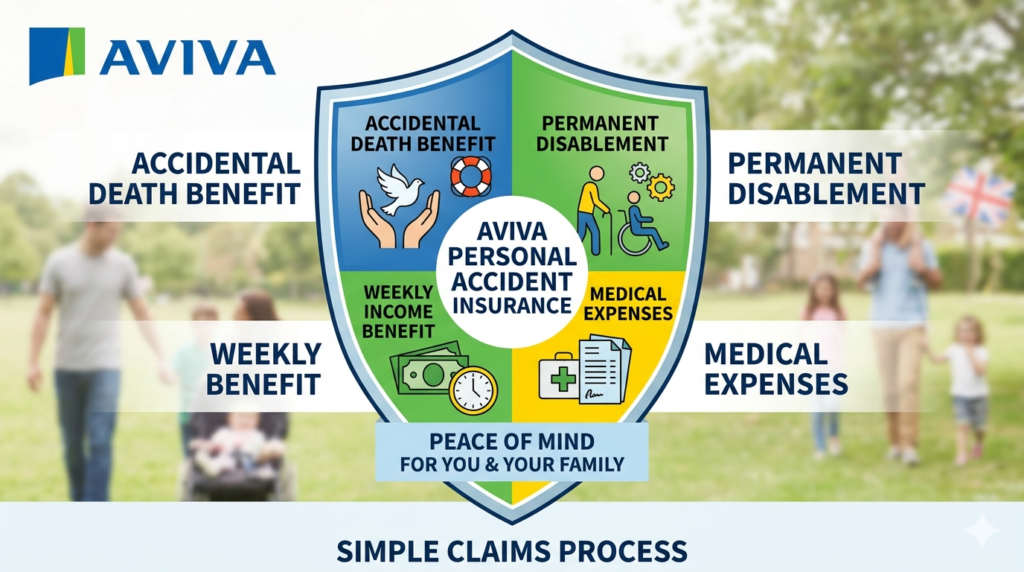

At its core, Aviva personal accident insurance is designed to provide immediate financial relief if you suffer a severe physical trauma. It is a contractual guarantee that if you sustain a specified accidental bodily injury, Aviva will pay you a tax-free lump sum of cash.

Unlike long-term Income Protection, which pays a percentage of your salary every month if you are signed off sick, a standalone personal accident policy is a much simpler product. It focuses exclusively on sudden, external, and unforeseen accidents.

Aviva generally offers this cover in two distinct ways:

- As a standalone policy: A dedicated, independent contract you buy specifically to cover yourself (and optionally, your family) against accidents.

- As an optional add-on: A supplementary upgrade attached to an existing Aviva motor, home, or life insurance policy.

Read our pillar page on Understanding the different types of accident cover

The Core Benefits: What exactly does Aviva pay out for?

When you review the schedule for Aviva personal accident insurance, the benefits are structured around a tiered payout system. The amount of money you receive depends entirely on the severity of the injury sustained.

While policy terms are updated regularly, Aviva’s cover typically provides financial support across these core categories:

1. Accidental Death

If an accident tragically results in a fatality, the policy provides a guaranteed lump sum to the deceased’s estate or family. This rapid injection of cash is vital for covering funeral expenses and providing an immediate financial buffer for grieving dependents before life insurance policies are fully processed.

2. Permanent Total Disablement (PTD)

This covers catastrophic, life-altering injuries. If an accident leaves you permanently unable to work in any occupation whatsoever (for example, due to a severe traumatic brain injury or complete paralysis), Aviva will pay out the maximum policy limit.

3. Specified Major Injuries

You do not have to be totally disabled to claim a substantial lump sum. Aviva personal accident insurance includes a schedule of fixed payouts for severe, permanent physical losses. These typically include:

- The physical severance or permanent loss of use of a limb (arm, hand, leg, or foot).

- The permanent and total loss of sight in one or both eyes.

- The total loss of hearing in one or both ears.

4. Broken Bones and Burns

Unlike some basic policies that only trigger for amputations or death, comprehensive Aviva cover often includes payouts for lesser, but still highly disruptive, injuries. This includes fixed cash sums for major fractures (such as a broken leg or pelvis) and severe third-degree burns.

5. UK Hospital Benefit

If your accident results in you being admitted to a UK hospital, the policy often provides a daily cash benefit (e.g., £50 a day). This helps cover the incidental costs of a hospital stay, such as travel expenses for visiting family members, parking fees, or emergency childcare.

What is excluded from Aviva personal accident insurance cover?

Understanding what an insurer will not pay for is arguably more important than knowing what they will. All insurance products contain strict exclusion clauses to prevent fraud and manage risk.

If you attempt to make a claim on your Aviva personal accident insurance under the following circumstances, it will be rejected:

- Sickness and Disease: This is a pure accident policy. It absolutely does not cover illnesses, viral infections, heart attacks, strokes, or any naturally occurring medical condition.

- Self-Inflicted Injuries: The policy will not pay out for intentional acts of self-harm or attempted suicide.

- Intoxication: If the accident occurred because you were under the influence of alcohol (above the legal driving limit) or illegal drugs, your cover is instantly voided.

- Hazardous Pursuits: Standard Aviva policies exclude high-risk sports. If you are injured while participating in professional sports, motorsport, extreme winter sports, or certain equestrian activities, you will not be covered unless you specifically declared these and paid for an upgrade.

- Illegal Acts: Any injuries sustained while committing a criminal offence are strictly excluded.

Read the Financial Conduct Authority (FCA) guidelines on transparent insurance exclusions

Who should seriously consider this policy?

While everyone benefits from a financial safety net, Aviva personal accident insurance is particularly valuable for specific demographics within the UK.

The Self-Employed and Sole Traders

If you are an independent plumber, electrician, or freelance consultant, you do not receive Statutory Sick Pay (SSP). If a broken wrist stops you from working, your income instantly drops to zero. A tax-free lump sum from Aviva provides the crucial emergency cash flow needed to pay your business lease, run your van, and feed your family while you recover.

Active Families

Children have accidents; it is a fact of life. Aviva often allows you to upgrade a single policy to a “Family Cover” package. This extends the protection to your spouse and dependent children. If your child breaks a bone at a playground and you have to take unpaid leave from work to care for them, the child’s fracture payout helps bridge that gap in your wages.

Those who cannot secure Income Protection

Comprehensive Income Protection is fantastic, but it is heavily medically underwritten. If you have a complex medical history (like previous battles with cancer or chronic conditions), you might be declined for Income Protection. Because Aviva personal accident insurance generally does not require a medical examination to set up, it offers a brilliant alternative way to secure at least some financial protection.

How to make a claim with Aviva

A major advantage of using a massive, established brand like Aviva is their streamlined infrastructure. If the worst happens, the claims process is generally straightforward and heavily digitized.

- Seek Medical Help First: Always prioritise your health. Go to A&E or your GP immediately.

- Gather Evidence: You will need undeniable proof of your accident and your injuries. This means requesting A&E discharge summaries, X-ray reports, or formal medical certificates.

- Notify Aviva Promptly: Do not wait six months to tell them. Call their UK-based claims team or log into the “MyAviva” online portal as soon as you are medically stable.

- Submit the Paperwork: You will be assigned a claims handler. Upload your medical evidence securely through their portal.

- Receive the Payout: Once the medical evidence satisfies the policy criteria, Aviva aims to deposit the tax-free lump sum directly into your bank account within a matter of weeks.

Read our step-by-step guide on How to successfully process a personal injury claim

Aviva vs. The Rest of the Market

Is Aviva the absolute best choice for you? It depends on your priorities.

The Pros: Aviva offers immense financial stability. They are not going to go bankrupt overnight, meaning your claim is secure. Their digital “MyAviva” app makes managing your documents and filing claims incredibly easy. Their inclusion of hospital cash benefits and fracture cover makes their policy more comprehensive than budget competitors.

The Cons:

Because you are paying for a premium brand name, their monthly premiums can sometimes be slightly higher than smaller, specialist brokers. Furthermore, if you work in a highly specialized, dangerous profession (like offshore rigging or working at extreme heights), an off-the-shelf Aviva policy might have too many occupational exclusions. In those cases, a specialist broker is required.

Frequently Asked Questions (FAQs)

1. Does Aviva personal accident insurance cover me if I am travelling abroad?

Usually, yes, but with limitations. Most standard policies will cover you 24/7, worldwide, for standard holidays. However, if you are travelling to a country where the Foreign, Commonwealth & Development Office (FCDO) has advised against all travel, or if you are moving abroad permanently, your cover will likely be invalidated. Always check your specific policy schedule.

2. Do I need to take a medical exam to get this cover?

No. One of the biggest benefits of Aviva personal accident insurance is guaranteed acceptance for most UK residents within the qualifying age bracket (usually 18 to 69). You do not need to provide blood tests, undergo a physical exam, or hand over your full GP records just to buy the policy.

3. Will claiming on this policy affect my other Aviva insurance?

No. If you have Aviva car insurance and a standalone Aviva accident policy, claiming for a broken leg on your accident policy will not suddenly increase your car insurance premiums. They are entirely separate legal contracts.

4. Is the payout from Aviva taxable in the UK?

If you pay the monthly premiums out of your own personal bank account using post-tax money, the lump sum payouts you receive from Aviva are generally completely tax-free. You do not need to declare this money to HMRC.

5. Can I cancel the policy if I change my mind?

Yes. UK insurance law grants you a standard 14-day “cooling-off” period. If you buy the policy, read the fine print, and decide it is not for you, you can cancel within the first 14 days for a full refund. After that period, you can usually cancel at any time without a penalty, though you will not get a refund for the months you have already used.

Conclusion

Building a robust financial safety net is about removing uncertainty from your life. A severe physical trauma is chaotic enough without the added terror of wondering how you will pay the council tax or put food on the table while you cannot work.

Aviva personal accident insurance offers a highly credible, stable, and well-structured solution to this problem. While it is vital to read the fine print regarding hazardous sports and occupational exclusions, the core product delivers exactly what it promises: rapid, tax-free financial relief when an accident shatters your routine.

If you are a self-employed professional, the primary earner in your household, or simply someone who wants to guarantee their family’s financial security, taking the time to review and secure this type of cover is an exceptionally smart financial move. Compare your options, calculate your survival budget, and secure the peace of mind you deserve today.

Pingback: What is Personal Accident Cover? The 2026 Ultimate UK Guide