Imagine sitting at your kitchen table on a quiet Sunday evening, sorting through your monthly bank statements. You spot a direct debit for an insurance policy you set up years ago, but suddenly, you cannot remember exactly what it protects. If you were severely injured in a car crash tomorrow and survived, would that policy step in to pay your mortgage? Or does it only pay out to your family if you pass away?

This confusion is incredibly common across the United Kingdom. When trying to build a robust financial safety net, the debate of personal accident vs life insurance is one of the most critical discussions you can have. Both policies are designed to provide a lump sum of cash during life’s worst moments, but they perform entirely different jobs, trigger under entirely different circumstances, and protect entirely different people.

If you choose the wrong policy, you could be left without an income precisely when you need it most. In this comprehensive guide, we will break down the complexities of personal accident vs life insurance, helping you understand exactly how they differ, how they overlap, and which cover you need to secure your family’s future and your current livelihood.

Table of Contents

Understanding the Core Difference: Personal accident vs life insurance

The easiest way to understand the core difference in the personal accident vs life insurance debate is to look at who receives the financial benefit and when that money is paid out.

At a fundamental level:

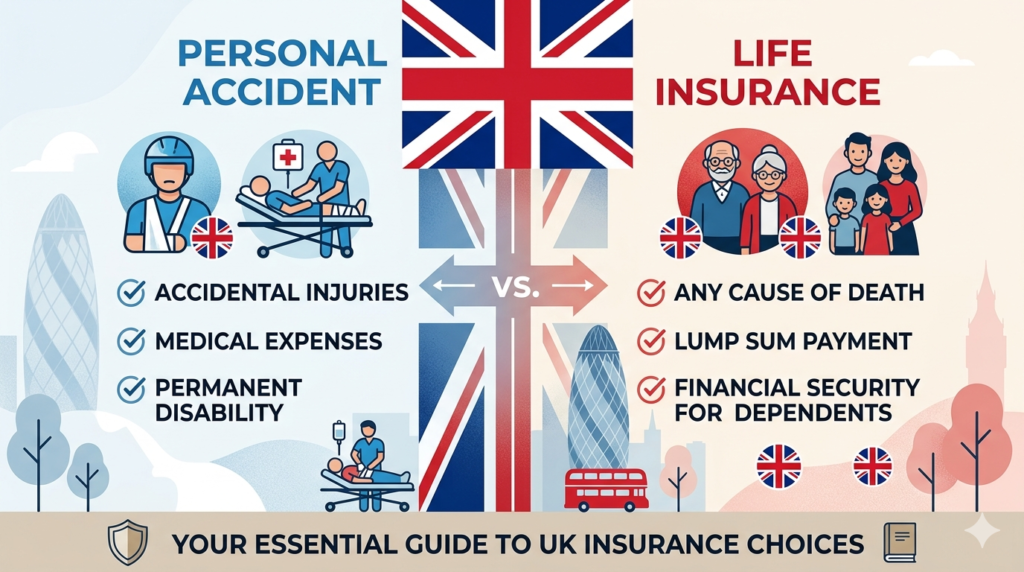

- Life cover is entirely selfless. It is designed to financially protect your dependents, your spouse, or your children after you have died. You will never see the money yourself.

- Accident cover is protective of your current lifestyle. It is designed to financially support you while you are still alive, but unable to work due to a severe physical trauma.

Let’s look closer at how each specific product functions in the UK market.

What is Life Insurance?

Life insurance is a highly structured financial contract between you and an insurance provider. In exchange for a regular monthly premium, the insurer guarantees to pay a substantial, tax-free lump sum of money to your nominated beneficiaries if you die during the term of the policy.

It acts as a financial replacement for you. It ensures that if your salary suddenly disappears forever due to your death, your family will not be forced to sell the house or struggle to pay for basic groceries.

The Triggers for a Payout

A standard UK life policy pays out for death caused by almost anything. Whether you pass away due to a sudden heart attack, a long battle with cancer, a viral infection, or a catastrophic road traffic collision, the policy will pay out. Furthermore, most good policies include a “Terminal Illness Benefit,” which pays the lump sum early if a doctor diagnoses you with less than 12 months to live.

Common Types of Life Cover

- Level Term Life: You pick a set timeframe (e.g., 25 years) and a set payout amount (e.g., £250,000). The potential payout stays exactly the same throughout the entire term.

- Decreasing Term Life: Often tied directly to a repayment mortgage. The potential payout decreases every year, exactly matching the decreasing debt on your home.

- Whole of Life: This covers you until the day you die, regardless of your age. Because a payout is a 100% mathematical certainty, these policies are significantly more expensive.

What is Personal Accident Insurance?

Where life cover focuses on the worst-case scenario of death, accident cover focuses on survival. It is designed to prevent financial ruin if you suffer a severe physical trauma that leaves you unable to earn a living.

When looking at personal accident vs life insurance, remember that accident cover is fundamentally about replacing your income and adapting your current living situation to a new physical reality.

The Triggers for a Payout

Unlike life cover, this policy only triggers if your injuries are caused by a sudden, external, unforeseen event. It does not cover illnesses or diseases. If you are diagnosed with a severe neurological disease, this policy pays nothing. However, if you fall from a ladder, suffer a severe burn, or lose your sight in a workplace incident, the policy leaps into action.

The Types of Financial Support

- Temporary Total Disablement (TTD): If you break your leg and cannot work for three months, the policy provides a regular weekly or monthly replacement income so you can keep paying your bills.

- Permanent Total Disablement (PTD): If your accident leaves you permanently unable to ever work again, the policy pays a large lump sum.

- Specified Injuries: It pays fixed lump sums for the permanent loss of limbs, loss of hearing, or loss of sight.

Read our pillar page on exactly how to calculate your ideal accident coverage amount

Key Comparisons: Personal accident vs life insurance

To truly make an informed decision, we need to place these two products side-by-side and examine how they handle specific scenarios. Here is a direct comparison of the rules governing both.

1. The Cause of Death

This is a massive distinction in the personal accident vs life insurance discussion. Life policies pay out regardless of how you die (illness or injury). Accident policies often include an “Accidental Death Benefit” which pays a lump sum to your family if you are killed in a crash or a fall. However, if you hold an accident policy and pass away peacefully in your sleep from natural causes, your family will receive absolutely nothing.

2. Medical Underwriting and Acceptance

When applying for life cover, you must undergo strict medical underwriting. You will be asked detailed questions about your family’s medical history, your weight, your smoking habits, and any pre-existing conditions. If you have suffered from severe depression or a heart condition, your premium will skyrocket, or you may be denied cover entirely.

Accident policies rarely require extensive medical underwriting. Because they only cover unforeseen external accidents, your family history of heart disease is irrelevant to the insurer. For individuals with complex medical backgrounds, weighing personal accident vs life insurance becomes heavily influenced by what they can actually get approved for.

3. The End Beneficiary

Life cover is placed into trust, and the funds bypass your estate to go directly to your spouse or children. You are purchasing a product exclusively for someone else’s benefit. Accident cover pays the money directly into your personal bank account. You use the funds to pay your own mortgage, adapt your car, or fund your own private physiotherapy.

Cost Analysis: Personal accident vs life insurance

When mapping out your monthly household budget, comparing the premiums of personal accident vs life insurance is an essential step.

Generally speaking, a standalone accident policy is significantly cheaper than a comprehensive life policy.

Why? Because statistically, humans are far more likely to pass away from an illness or a natural disease (which life cover pays out for) than they are to be killed or permanently disabled in a sudden accident. Because the insurer is taking on less mathematical risk with an accident policy, they can afford to charge you a much lower monthly premium.

If you are young, healthy, and do a desk job, life cover can be very affordable. But as you age, the cost of life cover increases dramatically. Conversely, the cost of accident cover often remains relatively stable, provided you do not suddenly take up extreme hazardous sports.

View the GOV.UK guidelines on planning your finances and managing debt

Do I Need Both? Resolving the Personal accident vs life insurance Dilemma

Rather than viewing personal accident vs life insurance as a strict either/or scenario, the most financially secure households in the UK view them as two halves of a complete safety net.

They complement each other perfectly. Relying on just one leaves a massive gap in your defences.

- Scenario A (Only Life Cover): You suffer a severe spinal injury in a fall. You survive, but you can never work again. Your life policy pays nothing because you are still alive. You lose your income and potentially your home.

- Scenario B (Only Accident Cover): You pass away from an aggressive illness. Your accident policy pays nothing because you were not involved in an accident. Your family is left without your income to pay the mortgage.

- Scenario C (Both Policies): If you are injured, your accident policy pays your wages and funds your recovery. If you pass away from an illness later in life, your life policy pays off the family mortgage. You are protected from every angle.

| Feature | Life Insurance | Personal Accident Insurance |

| Primary Trigger | Death (Any Cause) | Accidental Injury Only |

| Who Gets Paid? | Beneficiaries (Family) | You (The Policyholder) |

| Medical Exams | Strict Underwriting | Usually Not Required |

| Income Support | No (Lump sum only) | Yes (Weekly/Monthly benefits) |

Frequently Asked Questions (FAQs)

1. Which is better for a single person, personal accident vs life insurance?

If you are young, single, have no dependents, and rent your home, accident cover is usually the priority. Nobody is relying on your income to survive if you pass away, so life cover is less urgent. However, if you are injured and cannot work, you still need to pay your rent and buy food. Accident cover protects your current independence.

2. Does the taxation differ between personal accident vs life insurance payouts?

In the UK, both policies generally offer tax-free payouts, provided you pay the monthly premiums from your own post-tax personal income. However, life cover payouts can sometimes be subject to Inheritance Tax (IHT) if the policy is not properly written into a legal trust. Always consult a financial advisor to ensure your life policy is sheltered from IHT.

3. Is accidental death cover the main difference when comparing personal accident vs life insurance?

It is a major point of confusion. An accident policy usually includes an “accidental death” payout, but it is highly restricted. It only pays if death is directly caused by a sudden trauma (like a car crash). A true life policy pays out for death by any cause, including heart attacks, strokes, cancer, and old age.

4. Can I claim on both if I hold both personal accident vs life insurance?

Yes, in very specific tragic circumstances. If you hold both policies and you are tragically killed in a severe road traffic collision, your beneficiaries would likely receive the payout from your life policy, plus the accidental death lump sum from your accident policy. They are entirely separate legal contracts and holding one does not invalidate the other.

5. How do I choose between personal accident vs life insurance if I am on a tight budget?

If you have children and a joint mortgage, life cover must be your priority. The risk of leaving your family homeless is too great. Secure a basic decreasing term life policy to cover the mortgage first. Then, as your finances improve, you can add a budget-friendly accident policy later to protect your monthly income against short-term injuries.

Conclusion

The choice of personal accident vs life insurance is not about figuring out which product is inherently “better.” It is entirely about identifying the specific financial risks that keep you awake at night and purchasing the right tool to neutralize them.

If your primary anxiety is leaving your children or partner financially stranded after you pass away, life cover is your solution. If your primary anxiety is losing your own income, draining your savings, and struggling to survive following a severe physical trauma, accident cover is your safety net.

Navigating personal accident vs life insurance does not have to be an overwhelming process. Sit down, map out your current debts, look at who relies on your salary, and consider your daily risks. By understanding the distinct roles these policies play, you can confidently build a comprehensive financial shield that protects you in life, and protects your loved ones long after you are gone.

Pingback: Personal Accident and Sickness Insurance: The Essential UK Guide 2026