Imagine driving home from work on a dark, wet Tuesday evening. You are sitting at a red light, waiting patiently for the signals to change, when a distracted driver crashes into the back of your vehicle at speed. The sudden jolt leaves you with a severe neck injury and a fractured wrist. Your car is badly damaged, but more concerningly, your ability to work and earn a living is instantly stripped away.

While the term itself is often borrowed from American media, making auto accident claims in the UK is an incredibly common and strictly regulated process. Also known locally as road traffic accident (RTA) claims, this legal process is your primary route to securing financial justice. When you are injured through absolutely no fault of your own, knowing how to handle auto accident claims is the most important financial skill you can deploy.

Without a clear understanding of the law, you risk accepting a terrible early settlement offer, or worse, having your case thrown out on a technicality. In this comprehensive guide, we will break down exactly how auto accident claims work, the common mistakes to avoid, and the exact steps you must take to secure maximum compensation for your injuries and financial losses.

What are auto accident claims?

In the UK legal system, auto accident claims refer to the formal process of seeking financial compensation after a road traffic collision. They are pursued when you have suffered a physical or psychological injury, as well as financial losses, due to the negligence of another road user.

While your standard comprehensive car insurance deals with repairing the bent metal and replacing your damaged tyres, auto accident claims focus on repairing you.

It is vital to understand that pursuing auto accident claims correctly is a legal mechanism, not an automatic insurance payout. You must prove that the other driver breached their duty of care towards you on the road. The vast majority of auto accident claims in the UK are handled by specialist personal injury solicitors acting on a “No Win, No Fee” basis.

Read our pillar page on What is personal accident cover and how does it protect drivers

Common mistakes that ruin auto accident claims

Insurance companies are commercial businesses. Their primary goal is to protect their profit margins, which means they will actively look for reasons to reduce or deny your payout. Many victims accidentally ruin their own auto accident claims within the first 48 hours.

Avoid these critical errors:

- Apologising at the Scene: In British culture, saying “I’m sorry” is a reflex. However, saying sorry at the scene of a crash can be legally interpreted as an admission of guilt. Never admit fault. Simply exchange details and wait for the police or insurers to investigate.

- Toughing it Out: Adrenaline masks pain. If you feel “okay” and decide not to visit the hospital, you create a massive gap in your medical evidence. The opposing insurer will argue your injuries were not serious.

- Accepting the First Offer: Often, the at-fault driver’s insurance company will ring you days after the crash and offer a quick, low cash settlement to close the file. Never accept this without consulting a solicitor. It is almost always a fraction of what genuine auto accident claims are actually worth.

- Posting on Social Media: Do not post photos of your holiday, your gym routine, or your injuries on Facebook. Defence lawyers aggressively monitor social media to find evidence that contradicts your auto accident claims.

Immediate steps for successful auto accident claims

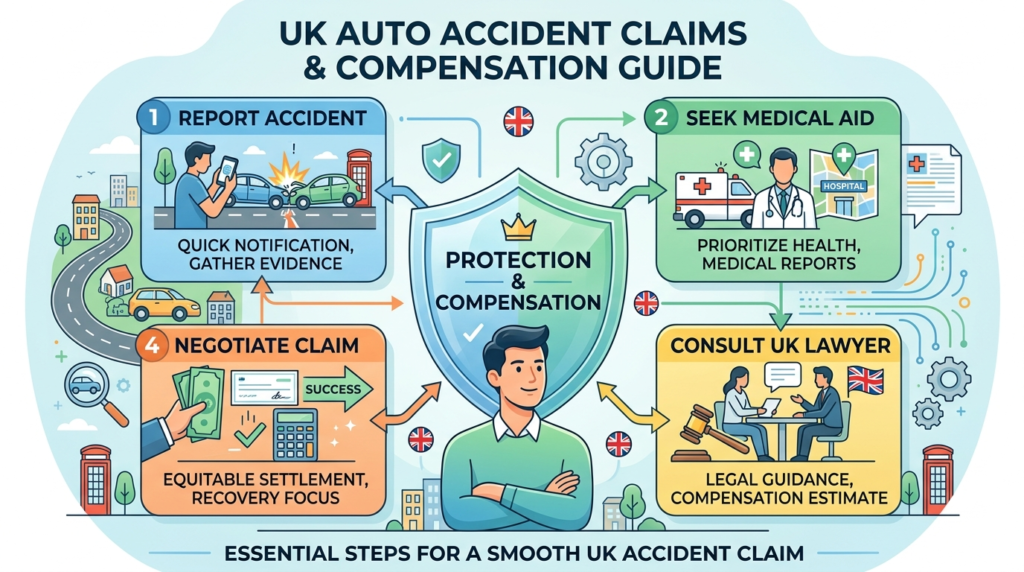

To guarantee you have the strongest possible case, the preparation for auto accident claims begins the very second the vehicles come to a halt. If you are physically able to do so safely, follow this strict protocol at the scene.

1. Ensure Safety and Call 999

Move to the side of the road or the pavement. If anyone is injured, or if the road is entirely blocked, you must call the police and an ambulance immediately. A formal police report is a highly powerful piece of evidence.

2. Exchange Details

Do not get into an argument about who caused the crash. Stay calm and collect the following from the other driver:

- Full name and home address.

- Vehicle registration number, make, and model.

- Their motor insurance provider and policy number.

3. Gather Undeniable Evidence

Your smartphone is your best tool for validating auto accident claims. Take wide-angle photos of the entire scene showing the position of the cars, road markings, and weather conditions. Take close-up photos of the damage to all vehicles. If there are any witnesses, politely ask for their names and telephone numbers.

4. Seek Medical Attention

Even if you only have a slight headache or neck stiffness, visit A&E, an urgent treatment centre, or your GP within 24 hours. Your medical records serve as the absolute foundation of your case.

First-party vs Third-party auto accident claims

Understanding the difference between the two main types of claims is crucial for securing immediate cash flow versus long-term wealth protection.

First-party claims

First-party auto accident claims are filed against your own insurance policy. For example, if you purchased a “Personal Accident Add-on” with your motor insurance, you claim directly from your own provider. This is a “no-fault” claim. It pays out a fast, fixed lump sum (e.g., £50,000 for a severe injury) regardless of who caused the crash. It is designed to pay your immediate mortgage and household bills.

Third-party claims

Third-party auto accident claims involve hiring a solicitor to sue the other driver’s insurance company. This is a fault-based legal claim. It takes much longer, but the financial payouts are entirely uncapped. It is designed to reimburse you for every single penny you have lost, and will lose, over the rest of your life.

The smartest strategy is to use both. Trigger your first-party insurance for immediate cash to survive, while your solicitor builds the third-party legal case for your ultimate compensation.

What compensation do auto accident claims cover?

A settlement is never a random, plucked-from-the-air number. Specialist solicitors calculate the value of high-tier auto accident claims by splitting the compensation into two distinct legal categories.

General Damages (For Physical Pain)

This category compensates you for your pain, suffering, and “loss of amenity.” Loss of amenity means the injury has stopped you from enjoying your life such as being unable to play your favourite sport or pick up your children. Solicitors use the Judicial College Guidelines, a strict legal directory, to value these physical injuries.

Special Damages (For Financial Loss)

This category is where auto accident claims secure your financial future. Special damages are designed to reimburse you for out-of-pocket expenses. You must keep all receipts to prove these losses. They include:

- Loss of Earnings: Your lost wages, missed overtime, and lost annual bonuses.

- Future Loss of Earnings: If you are disabled and must retrain for a lower-paying job, you can claim the difference in salary until retirement age.

- Medical Care: Costs for private physiotherapy, prescriptions, and specialist mobility equipment.

- Travel Expenses: Taxi fares to the hospital or mileage used travelling to medical appointments.

Read the official GOV.UK guidelines on Personal Injury Trusts and protecting your benefits

The impact of the UK Whiplash Reforms

If you are involved in a low-speed collision, you must be aware of the Civil Liability Act. The UK government introduced severe reforms in May 2021 specifically to crack down on fraudulent whiplash cases.

These reforms fundamentally changed how minor auto accident claims are processed:

- The Official Injury Claim (OIC) Portal: If your injuries are valued at under £5,000 (which covers most standard whiplash), you must submit your claim through a free government portal. You generally do not use a solicitor for this.

- Fixed Tariffs: Compensation for whiplash is now strictly capped by a fixed tariff system. For example, a minor neck injury lasting up to three months now commands a fixed payout of just £240.

- No Legal Fees Recovered: For these minor claims, you can no longer force the other side to pay your legal representation fees.

If you have suffered broken bones, head injuries, or any injury worth over £5,000, you are exempt from the portal and should immediately hire a “No Win, No Fee” solicitor.

How long do auto accident claims take to settle?

Patience is vital when dealing with civil law. There is no single timeline, as the speed of a settlement depends entirely on the severity of your injuries and whether the other driver admits fault.

Here is a general timeline you can expect:

| Claim Type | Liability Status | Estimated Settlement Time |

| Minor Whiplash (OIC Portal) | The other driver admits fault immediately. | 3 to 6 months |

| Moderate Injuries (Broken bones) | The other driver admits fault. | 9 to 18 months |

| Severe Injuries (Disability) | Liability is disputed or medical prognosis is unclear. | 2 to 4 years |

It is important that your solicitor does not rush your case. If you settle too early, and your injury suddenly gets worse a year later, you cannot reopen the case to ask for more money.

Frequently Asked Questions (FAQs)

Do auto accident claims usually go to court?

It is incredibly rare. More than 95% of auto accident claims in the UK are settled entirely out of court. Insurance companies want to avoid the massive costs and unpredictability of a judge’s ruling. Your solicitor will negotiate back and forth via letters and emails until a fair settlement is reached.

2. Is there a time limit for filing my claim?

Yes. The Limitation Act 1980 dictates that you have exactly three years from the date of the crash to either settle your case or officially issue court proceedings. If you miss this three-year deadline, you lose your right to claim entirely. Exceptions exist for children (they have until their 21st birthday) and those who lack mental capacity.

3. Are auto accident claims taxable in the UK?

No. General damages for your pain and suffering, as well as special damages for your financial losses, are completely tax-free. You do not need to declare your settlement money to HMRC as income or capital gains.

4. How do auto accident claims work with uninsured drivers?

If you are hit by an uninsured driver, or the driver commits a “hit and run” and flees the scene, you can still secure compensation. Your solicitor will submit your claim directly to the Motor Insurers’ Bureau (MIB). The MIB is a central fund, financed by a fraction of every legal UK car insurance premium, designed specifically to pay out in these exact scenarios.

5. Can I claim if the crash was partially my fault?

Yes, you can still claim under the rule of “split liability” or “contributory negligence.” For example, if the court decides you were 20% to blame because you were slightly over the speed limit when the other driver pulled out blindly, you can still win your case. However, your final compensation payout will be reduced by 20% to reflect your portion of the blame.

Read our guide on How to switch personal injury solicitors if you are unhappy

Conclusion

A sudden road traffic collision creates absolute chaos. It strips away your mobility, your income, and your peace of mind. While the legal jargon can feel overwhelming, mastering auto accident claims ensures that you are never left paying the price for another driver’s reckless behaviour.

By gathering undeniable evidence at the scene, seeking immediate medical care, and refusing early, low-ball settlement offers from aggressive insurers, you protect your rights. Most importantly, by instructing an accredited “No Win, No Fee” personal injury solicitor, you level the playing field against massive corporate legal teams.

Do not suffer in financial silence. If you have been injured on UK roads, take action today. Start gathering your paperwork, consult a legal professional, and ensure your auto accident claims deliver the full, uncompromising compensation you and your family deserve.

💡 Essential Reading for Your Claim

Before you proceed with your auto accident claim, make sure you understand the foundational rules of insurance in the UK.

Read the Ultimate Guide to Personal Accident Insurance →

Pingback: How to Find a Personal Accident Attorney in the UK: 5 Best Step Guide