Imagine walking through a local supermarket on a busy Saturday afternoon. A staff member has just mopped an aisle but forgotten to put out the yellow hazard warning sign. You slip on the wet tiles, fall awkwardly, and severely shatter your hip. The physical pain is intense, but as you wait for the ambulance, the financial reality hits you. You will be off work for six months.

As you return home and try to figure out your next steps, you are immediately confronted by a massive wall of legal jargon. The most common source of confusion for victims in the UK is understanding personal accident vs personal injury. Which one applies to your situation? Do you file an insurance claim, or do you instruct a solicitor to sue the supermarket?

Making the wrong assumption can leave you severely out of pocket and legally vulnerable. While these two terms sound identical, they serve entirely different purposes, trigger under entirely different circumstances, and deliver financial relief in very different ways.

In this comprehensive guide, we will break down the complexities of personal accident vs personal injury, explaining exactly how each system works, how they overlap, and how you can secure the maximum financial compensation to protect your family’s future.

Table of Contents

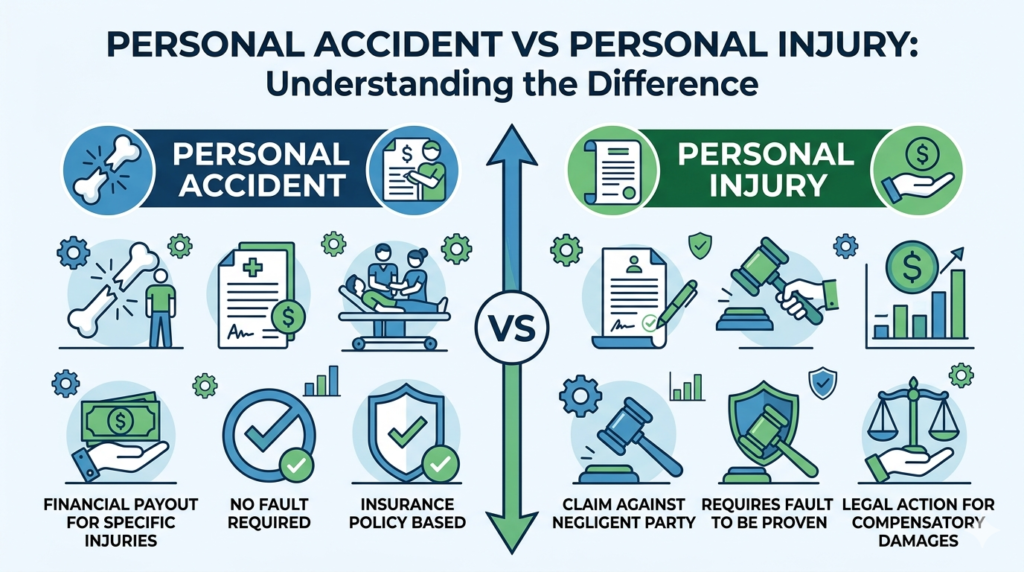

The Core Difference: Personal accident vs personal injury

When evaluating personal accident vs personal injury, the easiest way to understand the difference is to look at who is paying the money and why they are paying it.

- Personal Accident: This is a first-party insurance policy that you proactively bought for yourself before the accident happened. It pays out a pre-agreed sum of money regardless of whose fault the accident was. It is a contractual safety net.

- Personal Injury: This is a third-party legal claim against someone else. It is used when another person or organisation caused your accident through negligence. You hire a solicitor to sue their insurance company for tailored financial compensation.

The entire debate of personal accident vs personal injury rests on the concept of “fault.” Let’s look closer at how each specific route functions in the UK market.

Understanding Personal Accident Insurance

To truly grasp the dynamics of personal accident vs personal injury, we must first look at the insurance side of the equation.

Personal accident insurance is an optional financial product. You pay a monthly premium to an insurance provider to protect your income. If you suffer a sudden, unforeseen bodily injury, the policy pays out.

The “No-Fault” Principle

The most critical element in understanding personal accident vs personal injury is that personal accident cover is “no-fault.”

If you are riding your bicycle, lose your balance, and crash into a brick wall entirely through your own clumsiness, there is nobody to sue. However, your personal accident insurance will still pay out because an accident occurred. The insurer does not care if you were clumsy; they only care that you are injured and hold a valid policy.

Fixed Financial Payouts

This insurance does not care how much money you lost in total. It only pays out exactly what is written in your policy schedule. Payouts are generally structured in two ways:

- Temporary Total Disablement (TTD): If you break your arm and cannot work, the policy pays a fixed weekly sum (e.g., £400 a week) for a set period (e.g., 12 months) to replace your wages.

- Permanent Total Disablement (PTD): If you lose a limb or your sight, the policy pays a fixed, pre-agreed lump sum (e.g., £50,000).

Understanding Personal Injury Claims

Now we must examine the legal side of the equation. This distinction in personal accident vs personal injury matters because a legal claim is not something you buy in advance; it is a right you exercise after you have been wronged.

A personal injury claim is a formal legal action taken against a third party who breached their “duty of care” towards you. This means they were legally obliged to keep you safe, they failed, and you were injured as a direct result.

Proving Negligence and Fault

Unlike your insurance policy, a personal injury claim relies entirely on proving fault. If you fall down your own stairs at home, you cannot make a personal injury claim because nobody else is to blame.

However, if you are rear-ended by a speeding driver, or you trip over a severely broken council pavement, a third party is at fault. You instruct a solicitor to prove their negligence.

Tailored Compensation

In a legal claim, the payout is not a fixed, pre-agreed sum. It is meticulously tailored to your exact life circumstances. A solicitor will claim for:

- General Damages: Compensation for your physical pain, mental suffering, and loss of amenity (how the injury ruined your hobbies and lifestyle).

- Special Damages: A strict reimbursement of every penny you lost. This includes all your lost wages, future lost pension contributions, private medical bills, and travel expenses to hospital appointments. If your injury costs you £2 million over your lifetime, your solicitor will sue for £2 million.

Read the official GOV.UK guidelines on claiming compensation for a personal injury

Personal accident vs personal injury: A Direct Comparison

To make the best financial decision, you need to see the facts clearly. Here is a side-by-side view of personal accident vs personal injury:

| Feature | Personal Accident Insurance | Personal Injury Legal Claim |

| Nature of the process | An insurance contract claim. | A formal civil law dispute. |

| Do you need to prove fault? | No. Payouts happen regardless of blame. | Yes. You must prove a third party was negligent. |

| Who pays the money? | Your own insurance provider. | The at-fault party’s insurance provider. |

| How is the payout calculated? | Fixed limits agreed when you bought the policy. | Tailored exactly to your unique financial losses. |

| Do you need a solicitor? | No. You handle it yourself. | Yes. You need a “No Win, No Fee” lawyer. |

| How long does it take? | Very fast. Usually pays out within weeks. | Very slow. Can take 12 months to several years. |

The Overlap: Can you claim for both simultaneously?

This is where the overlap between personal accident vs personal injury becomes incredibly advantageous for victims.

Many people assume they have to choose one route or the other. This is entirely false. If you hold an insurance policy and someone else caused your accident, you can, and absolutely should, pursue both avenues at the exact same time. They are completely separate legal mechanisms.

When exploring personal accident vs personal injury, people often ask if claiming on their own insurance voids their right to sue. It does not. Here is how the two systems work together in perfect synergy:

The Synergy Scenario

Imagine you are a self-employed electrician. Another driver runs a red light and crashes into your van. You suffer a severe spinal injury.

- The Insurance Route: A legal claim will take two years to settle. You cannot wait two years to pay your mortgage. So, you immediately trigger your personal accident insurance. Within weeks, your insurer starts depositing £500 a week into your account. This stops you from going bankrupt.

- The Legal Route: At the exact same time, you hire a solicitor to sue the driver who ran the red light. Two years later, your solicitor wins the case and secures a £250,000 personal injury settlement to cover your long-term care and total lost career earnings.

Using both systems allows you to bridge the gap in personal accident vs personal injury timelines. The insurance provides the immediate emergency cash flow, while the legal claim secures your long-term wealth.

How to proceed if you have been injured

Navigating personal accident vs personal injury scenarios requires a cool head and immediate action. If you have just been involved in an accident, follow these exact steps to protect your rights on both fronts.

- Seek Immediate Medical Attention: Go to A&E or your GP immediately. Both your insurance provider and your solicitor will demand formal medical records to prove your injuries exist.

- Check Your Own Policies: Check your bank statements to see if you pay for a standalone accident policy. Also, check your life insurance, car insurance, and home insurance; many of these contain a small personal accident add-on.

- Notify Your Insurer Promptly: Insurance policies have incredibly strict notification deadlines (often 14 to 30 days). Call your provider immediately to lodge the fact that an accident has happened, even if you do not have all the medical paperwork yet.

- Preserve the Evidence: To succeed in the legal factor in the personal accident vs personal injury discussion, you need proof. Take photos of the accident scene, get witness phone numbers, and keep a diary of your pain and financial losses.

- Consult a Personal Injury Solicitor: Reach out to a “No Win, No Fee” lawyer. The initial consultation is always free. They will tell you immediately if your case has enough evidence to prove third-party negligence.

Read our step-by-step guide on How to make an insurance claim

Frequently Asked Questions

How does fault affect personal accident vs personal injury?

Fault is the dividing line. In an insurance claim, fault is irrelevant. Even if you caused the accident by not paying attention, your insurance policy will still pay your weekly benefit. However, in a legal claim, fault is everything. If the accident was 100% your fault, you have absolutely zero legal right to sue anyone else for compensation.

Which is faster in personal accident vs personal injury payouts?

Personal accident insurance is drastically faster. Because there are no arguments over who is to blame, and no lengthy court negotiations, your own insurer can begin paying your weekly benefit within just a few weeks of receiving your doctor’s “fit note.” A personal injury legal claim requires independent medical assessments and hostile negotiations with opposing insurers, meaning it regularly takes 12 to 36 months to receive a settlement cheque.

Are the payouts taxed in personal accident vs personal injury cases?

In the vast majority of scenarios in the UK, both payouts are completely tax-free. Personal injury legal compensation is legally exempt from income tax and capital gains tax. Similarly, if you pay your monthly personal accident insurance premiums out of your own post-tax bank account, the weekly payouts you receive are also tax-free.

Do I need a lawyer for personal accident vs personal injury?

You do not need a lawyer to claim on your own personal accident insurance; you simply fill out the forms provided by your insurer’s claims handler. However, you absolutely must hire a specialist personal injury solicitor to pursue a legal claim against a third party. Attempting to negotiate civil tort law and calculate Special Damages against a massive corporate insurance company without a legal expert will result in your case being severely under-settled or thrown out entirely.

Does my employer’s insurance cover both?

If you are injured at work, your employer’s “Employer’s Liability Insurance” handles the personal injury legal claim. You would sue that policy. Some highly generous employers also provide a “Group Personal Accident” policy as a staff perk. If they do, you could claim the immediate accident payout from HR, while simultaneously instructing an independent solicitor to sue the liability policy for your long-term damages.

Conclusion

When a sudden trauma turns your life upside down, financial panic is the absolute last thing you need. Clarifying personal accident vs personal injury is not just an exercise in legal definitions; it is about knowing exactly which weapons you have in your financial arsenal.

To summarise briefly: personal accident insurance is the safety net you proactively buy to catch you regardless of whose fault the fall was. A personal injury claim is the sword you use to demand full financial restitution from the person who pushed you.

Mastering personal accident vs personal injury ensures you are never left vulnerable. If you are injured, do not wait. Trigger your insurance policy immediately to secure your immediate cash flow, and consult a “No Win, No Fee” solicitor without delay to hold negligent parties accountable. By utilising both avenues, you ensure your recovery is focused entirely on your health, rather than your bank balance.